Simon Gwin @ simongwin99228 Member Since: 21 Feb 2026

United States

United States

About Me

The Essential Guide to Streamlining Construction Bond Approvals

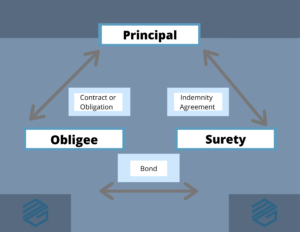

Understanding Surety Bonds and Their ImportanceSurety bonds are legal agreements between three parties: the obligee (the project owner), the principal (the subcontractor), and the surety (the bonding company). When a subcontractor secures a surety bond, they are essentially guaranteeing that they will complete the project according to the terms outlined in the contract. If they fail to meet those obligations, the surety company steps in to cover the financial losses up to the bond amount. This mechanism not only protects the project owner but also enhances the subcontractor's credibility.

Moreover, surety bonds help build trust with project owners. They demonstrate a contractor's commitment to completing projects as agreed and paying all involved parties. This commitment can lead to more opportunities for securing contracts, as project owners feel more secure knowing that they have a safety net in place. Additionally, successful bonding can result in better insurance terms and lower bonding costs in the future, further benefiting contractors.

Ignoring Market Trends

Another critical pitfall is ignoring prevailing market trends. Contractors must stay informed about the current state of the construction industry, including demand for bonding and shifts in surety expectations. Failing to adapt to these changes can result in missed opportunities or unfavorable bonding conditions.

Surety bonds serve as a guarantee that a subcontractor will fulfill their contractual obligations. This assurance is crucial for project owners who want to avoid potential financial losses due to non-completion or substandard work. Additionally, the process of obtaining a surety bond is often quicker and more accessible than many subcontractors realize. With the right information and preparation, subcontractors can navigate the bonding process smoothly and secure the necessary bonds to participate in larger projects.

The Importance of Thorough Documentation

Providing thorough and accurate documentation is essential for securing construction bonds. Missing or incomplete documents can lead to delays and even denials. When preparing your bond application, ensure that all required documents are present and well-organized. This includes financial statements, project references, and proof of insurance.

Bid Bonds: Navigating Requirements

Bid Bonds: Navigating Requirements Bid bonds are often required during the bidding process to ensure that contractors are serious about their proposals. The negotiation of bid bonds typically revolves around the amount of the bond and the requirements attached to it. Contractors should strive to understand the rationale behind the bond amount requested and negotiate terms that reflect their financial capabilities.

Payment Bonds: Ensuring Financial Security

Payment bonds are equally essential, as they guarantee that all subcontractors and suppliers will be paid for their work and materials. This bond protects against potential financial losses that may arise if a contractor fails to fulfill their payment obligations. For project owners, having a payment bond in place mitigates risks associated with contractor defaults.

Another essential strategy is to clearly articulate the contractor's value proposition. This includes showcasing unique strengths, such as a solid safety record, timely project completions, and financial stability. When sureties understand what sets a contractor apart, they may be more inclined to offer more favorable terms.

Another essential strategy is to clearly articulate the contractor's value proposition. This includes showcasing unique strengths, such as a solid safety record, timely project completions, and financial stability. When sureties understand what sets a contractor apart, they may be more inclined to offer more favorable terms. Another misconception is that contractors believe they can rush through the application process without sufficient preparation. This attitude can backfire, as surety companies scrutinize applications closely, looking for financial stability and project viability. A lack of preparation may lead to rejections or requests for additional documentation, further delaying the process and potentially jeopardizing project timelines.

Another misconception is that contractors believe they can rush through the application process without sufficient preparation. This attitude can backfire, as surety companies scrutinize applications closely, looking for financial stability and project viability. A lack of preparation may lead to rejections or requests for additional documentation, further delaying the process and potentially jeopardizing project timelines.How can I improve my chances of getting approved for a surety bond?

Improving your financial health, maintaining organized records, and providing thorough documentation can significantly enhance your chances of getting approved for a surety bond. Engaging with surety professionals for advice and maintaining good credit are also crucial steps.

Common Misconceptions About Bond Application Timing

Common Misconceptions About Bond Application Timing One prevalent misconception among contractors is that they can apply for surety bonds at any time and still receive favorable terms. In reality, the market conditions and the contractor's current project load can significantly affect the bond's cost and availability. Contractors often find that applying during peak seasons or when demand for bonds is high can lead to higher premiums or even limited options.

Understanding the right time to apply for surety bonds can significantly impact contractors' success in securing projects. Many contractors often make the mistake of applying too late or too early, which can lead to missed opportunities or unnecessary expenses. Timing is crucial in the surety bond process, and knowing the factors that influence the best time to apply can enhance a contractor's chances of approval and project success.

Understanding the right time to apply for surety bonds can significantly impact contractors' success in securing projects. Many contractors often make the mistake of applying too late or too early, which can lead to missed opportunities or unnecessary expenses. Timing is crucial in the surety bond process, and knowing the factors that influence the best time to apply can enhance a contractor's chances of approval and project success.If you liked this write-up and you would certainly such as to get more information regarding construction bond requirements kindly browse through our own page.

Rating

Freelancer Bridge: Connecting Talent and Opportunity. Our platform seamlessly links skilled freelancers with businesses and individuals seeking their expertise. Find the perfect match for your projects and unlock the potential of the gig economy today.